Hybrid, mobile, remote, and frontline work is shaping the UC&C market – and vendors will be shaping those work experiences in turn.

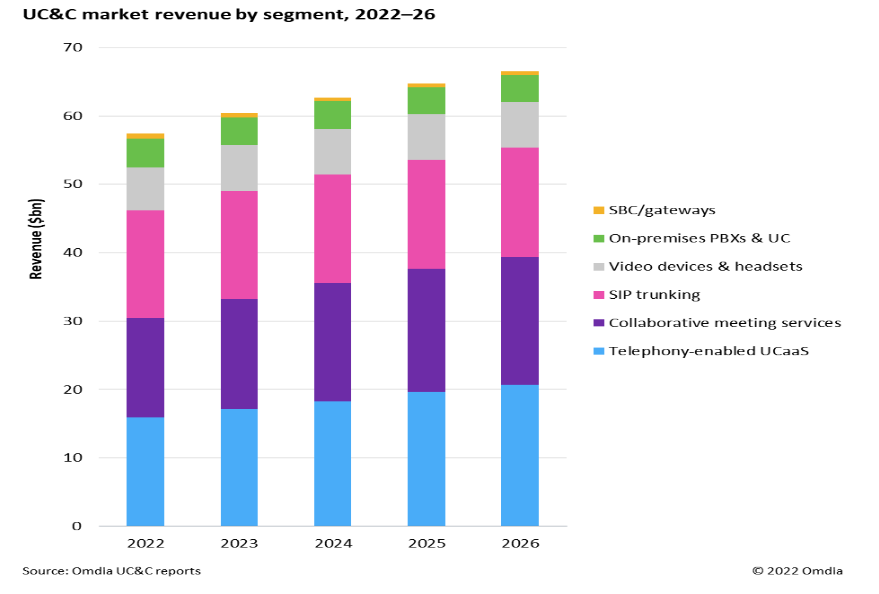

Cloud-based conferencing and collaboration technologies continued to lead the unified communications and collaboration (UC&C) market in 2022, building on the momentum they acquired during the pandemic. Omdia expects the UC&C market -- telephony-enabled unified communications as a service (UCaaS), collaborative meeting services, PBX, SBC, video conferencing endpoints, infrastructure and peripherals, and SIP trunking -- to be worth $57 billion in 2022. The overall UC&C market will stay resilient in 2023, despite the ongoing global macroeconomic challenges, and is expected to reach $66 billion by 2026.

So, what are the top UC&C trends to watch in 2023?

1. All eyes on UCaaS: The future of work is now for UC&C. UC&C underlies all hybrid, mobile, remote, and frontline work. Rapid platform development by the top UCaaS vendors will threaten smaller vendors, forcing them to reinvent themselves, move into adjacent markets, focus on specific verticals, and become an acquisition target. Omdia expects to see increased M&A activity in the UCaaS space in 2023. Top UCaaS vendors will continue competing on features but more on platform extensibility and their business adjacencies.

2. An oligopolistic market emerges: Omdia expects the UCaaS market to become an oligopolistic market in 2023. Only the top five vendors will control more than 70% of the revenue market share, forcing smaller point solution vendors to exit. We expect a moderate level of mergers and acquisitions activity in 2023, which will pave the way for this new market structure. In addition, the race to migrate the existing on-premises installed base to the cloud will pick up as the stakes are high, and vendors do not want to lose their customer base to the competitors.

3. Collaborative meetings offering will survive: Enterprises will start rolling out companywide UCaaS solutions for telephony, meetings, and messaging; however, preferences for collaboration tools will differ across departments, forcing businesses to have multiple UC&C solutions in 2023, primarily for inter-organization collaboration as dictated by their customers, partners, & suppliers. Thus, we will see enterprises leveraging two or more collaborative meetings and team collaboration platforms, their companywide UCaaS solution, and existing on-premises UC platforms.

4. On-premises PBX will persist in some industries: Organizations tend to keep their PBX even after significant numbers of employees have migrated to a cloud solution. Outages with major telephony-enabled UCaaS solutions this year are causing people to reconsider whether to retire the PBX. In addition, some organizations need rock-solid communications, even when all network paths to the outside world are down. This includes sensitive industries such as healthcare companies, educational institutes, and governments.

5. UCaaS vendors will seek adjacent market opportunities: Microsoft grew its UCaaS market share faster than any other vendor in 2021-2022, and it continues to dominate. Given the increasing threat from Microsoft, UCaaS vendors will try to create differentiation via new features and vertical-specific solutions and rapidly move into adjacent markets such as events.

6. Meeting devices market will lag: With the rapid adoption of hybrid work, the industry expected enterprises to quickly rip and replace their legacy meeting room solutions with the latest collaboration tools. There was a general expectation in 2022 that enterprises would adopt newer devices to offer equitable meetings in the hybrid setup. However, Omdia’s latest survey on video conferencing devices and services shows that enterprises will delay any significant reshuffle despite requirements for more video-enabled conference rooms. Enterprises in all regions will delay significant refreshes as they focus on improving operational efficiencies in 2023. Omdia expects single-digit growth in global shipments of endpoints in 2023 before a rebound in 2024. All-in-one videobars remain the market favorite and will see the highest shipment growth rate in 2023.

7. Equitable meeting experiences will get a reality check: No vendor has yet delivered a genuinely equitable meeting experience. Equitable meetings mean that every participant is treated equally, has the same screen real estate, and has an equal opportunity to be seen and heard wherever they are. In 2023, this market will see rapid innovation as vendors start leveraging artificial intelligence (AI) and multiple meeting room cameras in different form factors to support hybrid work delivery and equitable meeting experiences. AI will be at the center of new device innovations.

8. Device operating system will take center stage: All-in-one devices such as videobars and collaboration boards powered by Android- or Windows-based operating systems will drive the video collaboration market. Device vendors will incorporate sensors, pattern recognition, prediction, and other AI-based features to provide immersive user experiences.

9. Multiservice devices will start emerging: Meeting service-specific rooms (Zoom Rooms, Microsoft Teams Rooms, etc.) will continue to dominate in 2023 but will lose their appeal in hybrid work setups. Although video room systems optimized/certified for a specific vendor’s meeting service will constitute the bulk of device shipments in 2023, enterprises will gradually move away from dedicated meeting rooms such as Zoom Rooms and Microsoft Teams Rooms. This shift will lead to multiservice rooms, allowing employees to take any video meeting from any room, regardless of the service used.

10. New partnerships will shape the market landscape: We saw a few exciting partnerships in 2022, such as Cisco announcing a native Microsoft Teams experience on its Webex devices in collaboration with Microsoft. Since interoperability between meeting solutions is critical for enterprises, Omdia expects similar announcements from other vendors in 2023.

Finally, as a closing note, we expect to see continued spending in the UC&C market in 2023.